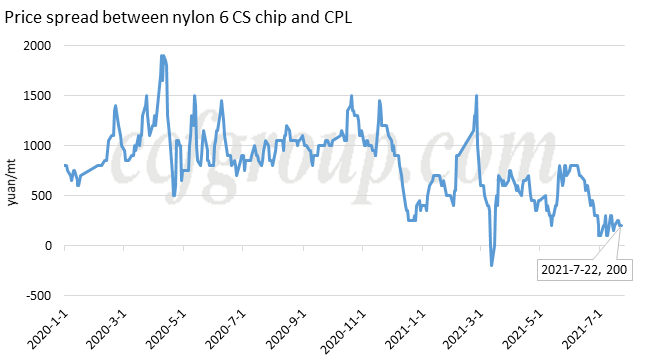

Coming to the end of July 2021, the price gap between nylon 6 conventional spinning (CS) chip and caprolactam has been narrowed to as low as 200yuan/mt. And consider cost difference between the payment (around 250yuan/mt), CPL RMB spot and nylon 6 CS chip spot price spread still lingers low around 450yuan/mt, the same low and profit-losing rate seen in early July. Nylon 6 CS chip plants have been through a difficult time, but they are about to go out of the worst time.

Demand for CS chip is recovering in Q3 2021

The demand for the conventional spinning chip in July has been obviously weak. Of its major downstream sectors, only cord fabric market has maintained a healthy status, but cord fabric plants only uses high-viscosity CS chip, which is independent from the majority, medium-viscosity CS chip.

Medium-viscosity CS chip market has three major downstream sectors: modified plastics, staple fiber and film.

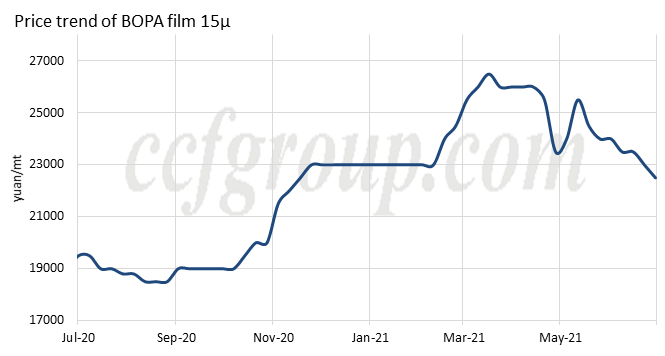

Film: Prices of BOPA film 15μhas been falling since June and continued through July. Its related end user’s market, food packaging was not as good as the previous year. However, film plants are still certain about returning orders in the third quarter of 2021, and they maintain optimistic look toward August.

Major film plants including Yuncheng and Changsu have replenished a great volume of nylon 6 CS chip in May, when chip market hit low at 14,000yuan/mt, and this large amount of feedstock preparation has hindered their restock for CS chip in June-July. But chip stocks in BOPA film plants are about to be consumed out, and the new round of replenishment is underway in August.

Modified plastics: Sales of modified plastic plants has been reducing month-on-month since May, so is their purchasing of nylon 6 CS chip. The global crunch in micro chip is the major reason for reduced plastic sales, since a prominent part of nylon-based modified plastics is applied to make automobiles. But according to China Association of Automobile Manufacturers, the supply shortage in chip has peaked in the second quarter and will gradually be eased in the rest of the year. Automobile production is forecasted to recover in August as well, and the sales and purchasing of modified plastic plants will resume as well.

Staple fiber: The performance of nylon staple fiber market has been relatively neutral since July, and the general development is similar with the textile industry, which means the forecast toward Q3 is positive as well. Or at least, it will not become a short board in CS chip market.

Demand of the three largest downstream sectors of medium-viscosity CS chip is not going to worsen any more in short, and their outlook is in general positive toward the third quarter.

Feedstock cost pressure will ease

On the raw material side, caprolactam market has maintained a tight balance in July still, as the restart of part of plants and the startup of several new capacities have been delayed. Supply and demand pattern in East China remains balanced. But this situation will not last long, since near one million tons/year of new CPL capacities are expected to commence in the latter half of the year, and the process is starting in August. With the scheduled new capacities released, CPL supply will be evidently ample and that will weaken CPL plants’power in negotiating the price with downstream, and in another word, chip plants will have more advantage in the trade with their raw material suppliers.

Chip plants' stock, run rate and future development

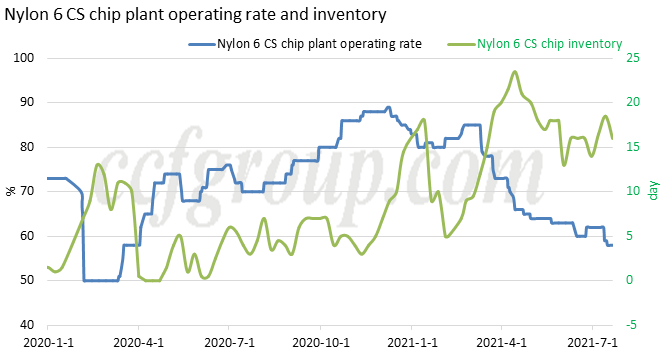

After long-term of consolidation, nylon 6 CS chip plants have suffered heavy deficits, the pressure is huge for this industry, despite of different method taken by plants to cope with it. CS chip plants have almost reduced their operating rate to the lowest in late July, to 58% of the total capacity only. The average chip inventory has kept around half a month.

The inventory rate is not giving chip plants a light start in August, but it is not a big threat either. (Some polymer makers have intentionally kept some stocks for the peak season even.) Above all, from feedstock cost, demand performance and nylon 6 CS chip plants’operation pressure, they are likely to recover in the rest time of the third quarter.